Bitcoin Mining

🧰Services

ID: 320

20,059.10USDC

Open

66.86% of 30,000 USDC

- Loan period8 months

- Lending APR23.10 %

- Expires22 days, 23:54:37

About

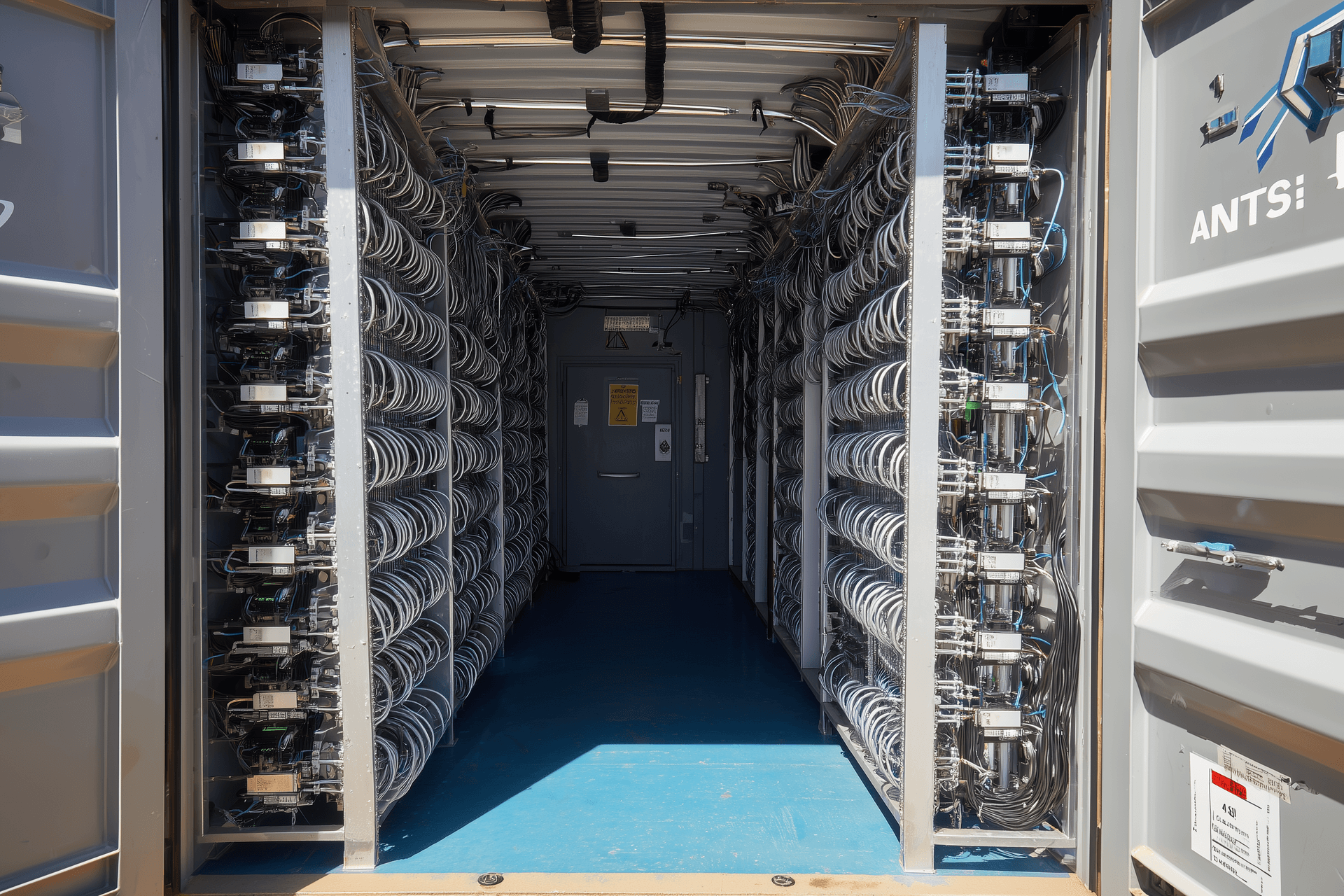

ORAX Assets Management Corp. is a Panama-incorporated international business corporation with operating assets located in Paraguay. The company has been created as a dedicated vehicle for industrial-scale Bitcoin mining, built around a single, expandable site connected to the Paraguayan electricity grid. ORAX’s core activity is the ownership and operation of ASIC-based mining capacity for its own account, with a strategic emphasis on accumulating mined BTC on the balance sheet (“mine-and-hold”) rather than treating it as short-term operating cash flow.

The current site utilises approximately 2 MW of electrical load through installed mining hardware and 24/7 secured operations. Electrical and physical infrastructure have been prepared for a ramp-up to about 8 MW, with contractual potential to reach 8–10 MW under the existing tariff framework. At this stage, the primary bottleneck for growth is hardware and financing, not power or space: the site is conceptually framed as a concentrated, scalable platform for low-cost BTC production using modern, optimised ASIC fleets.

Business model and activities

ORAX operates as a pure-play self-miner rather than a hosting provider or hardware reseller. Its business model is to secure structurally low-cost grid electricity in Paraguay, deploy its own ASIC machines under an optimised air-cooled setup and convert power into BTC at the lowest achievable all-in unit cost. Value accrues entirely to the company’s own balance sheet: there are no third-party clients whose machines are hosted on site, and no fee-based services that would dilute the economic upside from mining.

The platform integrates the full mining value chain for proprietary operations: selection, procurement and import of ASIC hardware; sea freight and customs; pre-deployment preparation (inspection, replacement of selected components, thermal management); installation and configuration in racks; firmware optimisation; continuous monitoring; on-site maintenance and repairs. A key differentiator is the systematic use of customised firmware targeting a 15–20% uplift in computing performance versus stock settings, enabling higher hashrate per unit of invested capital and per kWh consumed.

On the financial side, ORAX’s activities are anchored in a “mine-and-hold” treasury policy. Mined BTC is treated as a strategic treasury asset and is not systematically sold to cover operating expenses. Instead, part of the BTC balance is pledged as collateral for loans (typically up to ~50% loan-to-value), with funding received in USDT at interest rates in the 6–8% p.a. range. These loans are used to finance operating costs, allowing mined coins to be retained and positioning the company to benefit from potential price appreciation, particularly around and after the expected 2028 halving.

Operating structure

Operationally, ORAX combines a lean internal core with extensive use of specialised contractors. The in-house team handles strategic management, key technical decisions and day-to-day operation of the Paraguayan site: hardware selection and procurement, logistics coordination, firmware deployment, performance monitoring, repairs, preventative maintenance and basic administration. Four operators work on site under the supervision of a COO, supported by the founder and a small administrative/PA function that manages documentation flows and coordination with lenders, suppliers and service providers.

Construction and electrical works for the site build-out, 24/7 physical security, international logistics and customs clearance, as well as accounting, tax and legal support are handled by external partners. The site runs under a three-year fixed-price electricity supply contract with the local grid operator, and its physical layout is optimised for high-density air-cooled ASIC deployments, with an emphasis on airflow management, heat evacuation and uptime. This “light” structure keeps fixed overheads relatively low while allowing the company to scale installed hashrate primarily through additional hardware purchases rather than repeated infrastructure build-outs.

Clients and market position

Unlike many mining companies that combine self-mining with hosting, ORAX deliberately operates without external clients. All hashrate at the site is owned and controlled by the company itself, and there is no sales or marketing function aimed at attracting retail or small institutional miners. Management does not see a strategic rationale for working with small “retail” customers (1–10 machines) and wishes to avoid the complexity of managing numerous small accounts.

In principle, the infrastructure and operating model could be extended to large-scale hosting or joint-venture arrangements with institutional partners, particularly if by March–April 2026 the platform has not been fully populated with ORAX’s own hardware. Any such services would be treated as supplementary to the core self-mining strategy. In the broader market, the company positions itself as a cost-focused, hydro-powered miner in Paraguay, aiming to sit toward the lower end of the global cost curve with an all-in BTC production cost in the mid-30k USD/EUR-equivalent range at 8 MW, under current assumptions.

Leadership and organisation

The strategic concept and current profile of ORAX are closely tied to its founder and sole shareholder, Goran Jovanovic, a Bitcoin enthusiast since 2011 with prior experience as an investor in publicly listed mining companies such as Bitfarms and other sector peers. His long-term engagement with the ecosystem has shaped the company’s focus on cheap power, high uptime, firmware-driven optimisation and disciplined capital allocation.

In 2025 he transitioned from purely financial exposure to building his own physical operation, leading the securing of land and grid connection in Paraguay, the negotiation of the three-year fixed-price power contract and the design and build-out of the initial 2 MW infrastructure. He remains the key decision-maker for strategy, expansion, treasury policy and risk. A small management and administrative team supports him in Panama and on the ground in Paraguay, while non-core functions are outsourced. As a result, ORAX currently presents as a focused, founder-driven mining platform with tangible infrastructure and clear scaling potential, but with typical early-stage characteristics: high key-person dependence, single-site concentration and full exposure to Bitcoin’s long-term price and difficulty trajectory.

Loan Collateral

The EUR 3,600,000 capex facility is secured by hard, productive mining assets at ORAX’s Paraguayan site. The collateral package consists of:

existing, fully built-out electricity and site infrastructure and the already installed ASIC fleet at the current 2 MW configuration;

all new mining hardware and associated infrastructure purchased with the loan proceeds to add c. 6 MW of capacity (bringing the site to 8 MW).

Given the specific nature of mining assets, collateral is presented at two levels:

Base value – book / purchase value in EUR;

Conservative liquidation value – 90% of base value (10% haircut), reflecting that installed, operational ASICs and infrastructure typically retain strong resale value, as they can generate cash flow immediately when powered.

On this basis, pledged assets provide collateral coverage of the loan principal of approx. 154% at base value and 139% on a 10% haircut basis.

Collateral summary

Collateral source | Base value (EUR) | Liquidation value, 90% (EUR) |

Existing site infrastructure and installed fleet | 1,956,039 | 1,760,435 |

Loan-financed hardware and infrastructure | 3,600,000 | 3,240,000 |

Total collateral | 5,556,039 | 5,000,435 |

Coverage indicators

Base value coverage: EUR 5,556,039 vs. EUR 3,600,000 ≈ 154%

Liquidation value coverage (90% of base): EUR 5,000,435 vs. EUR 3,600,000 ≈ 139%

Thus, even under a conservative 10% haircut on all pledged assets, the collateral base still exceeds the loan principal by a substantial margin. All pledged items are core, income-generating components of the mining operation. In addition, ORAX plans to build and maintain a BTC treasury under its mine-and-hold strategy; these BTC holdings primarily secure short-term BTC-backed operating loans and are not included in the tables above, but represent an extra economic buffer beyond the hard-asset collateral package.

Highlights

Max target

30,000 USDC

Min target

15,000 USDC

Investors

47

Interest payments

8 months

Principal repayments

bullet

Total payments

monthly

Risk scoring

- CollateralCompany Assets

- Total risk scoreA

- Debt to equity1.6

- LTV72 %

- Credit history8/10

Details

ORAX’s available financial data cover the first three months of commercial operations at its Paraguayan site (September–November 2025). Over this period, the company has demonstrated strong gross and operating margins on a relatively small but growing revenue base, confirming the economic viability of the 2 MW configuration under the current power tariff and network conditions.

All figures below are expressed in EUR, converted from USD at an illustrative rate of 1 USD = 0.86 EUR.

Key financial indicators

(Values in EUR ’000, rounded)

Period | Revenue | Gross profit | Net profit* | Gross margin | Net margin |

Sep 2025 | 51 | 39 | 32 | 75% | 63% |

Oct 2025 | 145 | 103 | 90 | 71% | 62% |

Nov 2025 | 118 | 77 | 61 | 65% | 52% |

Sep–Nov 2025 | 315 | 219 | 183 | ≈69% | ≈58% |

Revenue recognition follows the company’s mine-and-hold approach: monthly revenue is calculated as the end-of-month BTC price multiplied by the BTC mined in that month, without requiring actual BTC sales. This is a mark-to-market representation of economic value created, rather than realised cash income.

Analysis of revenue and profitability

In September 2025, the first month of the presented period, ORAX generated around EUR 51k of revenue with a gross margin of 75% and an approximate net margin of 63%. This reflects a small but efficient operation at 2 MW, with a lean cost base and limited fixed overhead.

In October 2025, revenue almost tripled to about EUR 145k, driven by higher BTC production and pricing, while gross and net margins remained very strong at roughly 71% and 62% respectively. This indicates that the cost structure scaled well with increased output, and that additional revenue largely fell through to operating profit.

In November 2025, revenue moderated to approximately EUR 118k, broadly reflecting BTC price movements and normal month-to-month volatility. Gross margin eased to around 65% and net margin to roughly 52%, but the operation remained highly profitable on an economic basis.

Across the three months combined, ORAX generated:

Revenue of roughly EUR 315k

Gross profit of about EUR 219k

Net (operating) profit of approximately EUR 183k

This corresponds to an overall gross margin of about 69% and a net margin of about 58% for the period.

Key trends and financial observations

The first three months of data show a profitable early-stage profile with very high percentage margins, consistent with a low direct power cost and a compact organisational structure.

Gross and net margins naturally fluctuate with BTC price and network conditions, but the spread between the all-in cost of production per BTC and the mark-to-market value of mined BTC is substantial in this period. On a unit basis, the internal calculations for September–November indicate an all-in production cost (power + services + overhead) of roughly EUR 36–37k per BTC, compared with an average realised value of around EUR 88k per BTC equivalent, implying an economic margin on the order of 58%.

Operating expenses are modest in absolute terms and remain low relative to revenue, reflecting a lean in-house team and outsourcing of non-core functions. This supports strong operating leverage: as capacity and BTC production increase, ORAX expects a significant portion of additional revenue to translate into incremental operating profit, provided power tariffs and network conditions remain broadly in line with current assumptions.

At the same time, the financial track record under the current model is very short (three months), and results are inherently sensitive to BTC price, difficulty and uptime. The current figures should therefore be viewed as an initial proof of concept for the 2 MW setup and the chosen mine-and-hold approach, rather than as a fully representative sample across different stages of the Bitcoin cycle.

Growth Plan

ORAX is currently in the early phase of scaling its Paraguayan platform. The site is operating at approximately 2 MW of active load, while the underlying electrical and physical infrastructure has been designed and prepared to support a gradual ramp-up to around 8 MW, with technical potential to reach 8–10 MW under the existing power framework. The platform is used exclusively for proprietary mining; no third-party hosting capacity has been commercialised to date.

The core development path for the company is therefore straightforward: first, to fully utilise the existing site up to its 8 MW design capacity, and second, where feasible, to explore further expansion of the available electrical capacity on similar economic terms. In other words, growth is defined primarily as the progressive “filling” of the current location with additional ASIC hardware, rather than as geographic diversification or a shift into client-hosting services.

Strategically, ORAX intends to follow a consistent sequence: mine BTC, hold it on the balance sheet, use part of this BTC as collateral for loans to cover operating expenditure, and build capacity ahead of the expected 2028 halving. The company explicitly does not plan to systematically sell mined coins to finance day-to-day operations. Instead, operating costs are expected to be funded largely through BTC-backed loans disbursed in USDT and, where appropriate, additional mining-oriented financing, allowing BTC holdings to grow through the cycle.

This approach is anchored in management’s view of the next halving cycle. ORAX’s planning assumes that by the time of, and especially after, the 2028 halving, the Bitcoin price will reach at least USD 125,000 per BTC. The company’s objective is to enter that period with a fully built-out 8 MW site, a modern ASIC fleet and a substantial BTC reserve accumulated at a structurally low unit cost. Once the targeted post-halving price levels are reached, ORAX expects to sell only the portion of its BTC necessary to repay outstanding loans and interest, retaining the remaining coins and the physical infrastructure as long-term assets.

Within this context, debt financing – particularly BTC-backed lending – is viewed as the primary growth channel because it allows ORAX to keep all of the mining margin and upside. Hosting large external clients is considered a secondary, optional lever that would be activated only if, by a defined internal deadline, the platform cannot be fully filled with the company’s own equipment. Even in that case, such arrangements would be designed as complementary to, and not a replacement for, the core mine-and-hold growth strategy.

Projected BTC accumulation over the 14-month 8 MW phase

Once ORAX scales its Paraguayan site to 8 MW of active load, management expects the mining operation to stabilise at roughly 6.06 BTC per month under current network conditions. In the base planning case, the company assumes a reference BTC price of USD 90,000 (≈EUR 77,400) for internal mark-to-market of monthly production and structures operating financing around that level.

Monthly BTC production and operating financing at 8 MW

Metric | Value / Assumption | Per month (USD) | Per month (EUR*) |

BTC mined | Fixed hashrate at 8 MW | 6.0633448 BTC | – |

BTC price (for monthly valuation) | Scenario input | 90,000 | 77,400 |

Value of BTC mined | 6.0633448 × 90,000 | 545,701 | 469,303 |

Cash production cost | Power + operating inputs | 222,742 | 191,558 |

BTC-backed operating loan | Loan in USDT secured by BTC | 222,742 | 191,558 |

In practical terms, each month at 8 MW ORAX:

mines about 6.06 BTC,

recognises a production value of about USD 545.7k / EUR 469.3k (at USD 90k/BTC), and

requires approximately USD 222.7k / EUR 191.6k of cash to cover direct production and operating costs, funded via a BTC-collateralised loan in USDT.

Consistent with the mine-and-hold strategy, ORAX’s intention is not to liquidate the entire BTC balance to realise this surplus. Instead, the company expects to:

sell only as many coins as necessary to repay all loans and interest once the targeted price level (≥USD 125k/BTC) is reached;

retain the remaining BTC as a long-term treasury asset; and

continue using part of the BTC reserve as collateral for future operating loans, while owning outright both the 8 MW infrastructure and the associated mining hardware fleet.

Alternative financing route and contingency repayment scenario

In parallel to the base-case 14-month facility, ORAX is also evaluating an alternative financing option under tighter terms, namely a shorter-tenor loan with an indicative interest rate of 23.1% p.a. and an 8-month maturity. Under this structure, management expects that during the 8-month operating window the expanded capacity would allow the company to repay approximately 50–55% of the total repayment obligation (principal plus accrued interest) from operating profit generated over the period, while maintaining the mine-and-hold approach as the core treasury framework.

For the remaining balance at maturity, ORAX considers two practical repayment paths.

Asset sale scenario. If required, the company can sell a portion of the newly acquired ASIC fleet. Mining hardware of the S21-class is globally traded and remains liquid in secondary markets, particularly when equipment is already installed and operational. Under this scenario, the expected resale value of the purchased equipment is intended to cover the residual repayment amount without relying on future BTC price appreciation.

Bank refinancing scenario. As an alternative, ORAX can refinance the short-term loan through a conventional bank facility once the expansion is executed and the asset base is fully reflected on the balance sheet. At that stage, the company expects to have sufficient tangible collateral in the form of mining infrastructure and equipment to support a materially lower-cost facility, with collateral coverage (fixed assets versus new borrowing) exceeding 250%, improving lender comfort and reducing pricing versus the initial short-term instrument.

Description of the Loan

ORAX Assets Management Corp. is seeking a capex facility of EUR 3,600,000 to finance the expansion of its Paraguayan mining site from approximately 2 MW to 8 MW of active electrical load. The loan is intended exclusively for the purchase, import and deployment of additional ASIC mining equipment and related site adaptations, corresponding to roughly 6 MW of incremental capacity. The facility is not designed to refinance historical losses or fund ongoing operating expenses; those are expected to be covered through BTC-backed working-capital loans secured against mined BTC.

Purpose and use of proceeds

Loan proceeds will be used to finance:

acquisition of approximately 1,710 Bitmain Antminer S21 PRO units (or machines of similar efficiency class) corresponding to the additional 6 MW;

international logistics and customs clearance for these units (sea freight, insurance, brokerage, local transport);

installation, racking, power distribution and network integration at the Paraguayan site;

initial servicing, spare parts and minor site adaptations needed to operate the expanded 8 MW configuration.

In substance, the facility bridges the capital requirement between ORAX’s existing 2 MW infrastructure and the fully built-out 8 MW setup on which the company’s financial projections and growth plan are based.

Alternative financing option

ORAX is prepared to consider an alternative structure with a shorter maturity and a higher coupon. This option is intended as a pragmatic execution path if the lender prefers faster capital turnover and earlier de-risking through shorter duration.

Alternative option – indicative terms

Parameter | Base-case facility | Alternative facility |

Total facility amount | EUR 3,600,000 | EUR 3,600,000 |

Purpose | 6 MW expansion to reach ~8 MW total load | Same |

Tenor | 14 months | 8 months |

Interest rate | 14% fixed p.a. | 23.1% fixed p.a. |

Interest payments | Monthly | Monthly |

Principal repayment | Bullet at maturity | Bullet at maturity |

Tranches | 6 × EUR 600,000 | 6 × EUR 600,000 (or as agreed) |

Under the alternative 8-month, 23.1% p.a. structure, management expects that the expanded capacity would allow ORAX to cover a material portion of the overall repayment obligation during the operating window through operating profit, reducing end-of-term dependence on BTC price appreciation. Any remaining balance at maturity can be addressed via the company’s contingency paths described in the growth-plan section, including partial resale of newly acquired ASIC equipment (highly liquid secondary market) or refinancing through a conventional bank facility once the expanded asset base is fully reflected on the balance sheet.

Key facts

- ORAX ASSETS MANAGEMENT CORPORATION was foundedSep 02, 2025

- Start of active work/productionSep 10, 2025

Borrower info

ORAX ASSETS MANAGEMENT CORPORATION

Panama City, 1801, 18th floor at Global Bank Tower, 50th Street, P.O.Box 55-2484

ORAX Assets Management Corp. is a Panama-incorporated international business corporation with operating assets located in Paraguay. The company has been created as a dedicated vehicle for industrial-scale Bitcoin mining, built around a single, expandable site connected to the Paraguayan electricity grid. ORAX’s core activity is the ownership and operation of ASIC-based mining capacity for its own account, with a strategic emphasis on accumulating mined BTC on the balance sheet (“mine-and-hold”) rather than treating it as short-term operating cash flow.

- Reg No.155772436

Market description & size

Global Bitcoin mining environment

Bitcoin mining is a large, capital- and energy-intensive industry where competitiveness is driven primarily by electricity cost, hardware efficiency and uptime. Over the last years hashrate has grown rapidly, pushing inefficient, high-cost miners out of the market and favouring operators with cheap, stable power and modern ASIC fleets. Regions with abundant hydro or other low-cost generation (including parts of Latin America) have become natural hubs for industrial-scale mining.

Halving and its implications

Bitcoin’s block reward has already passed four halvings (2012, 2016, 2020, 2024), each time cutting miner rewards per block by 50%. Historically, halvings have tightened miner economics while often being followed by medium-term BTC price appreciation, though with differing magnitude each cycle. The next halving, expected around 2028, will again reduce block rewards and is likely to increase pressure on high-cost producers, making low unit cost and strong balance-sheet BTC reserves particularly important.

Positioning of ORAX within this context

Within this environment, ORAX positions itself as a focused, low-cost self-miner in Paraguay, leveraging hydro-based grid power under a fixed-price contract and optimised ASIC fleets. The company’s strategy is to scale a single site to 8 MW, mine BTC at a structurally low all-in cost, and follow a mine-and-hold treasury policy supported by BTC-backed loans. This positions ORAX to potentially benefit if BTC reprices upwards into and after the 2028 halving, while remaining exposed to the usual sector risks of BTC price, difficulty and single-site concentration.